Planning your retirement is one of the biggest financial decisions you will ever make. When it comes to Social Security benefits, timing matters a lot. Many people don’t realize that claiming early can reduce their monthly income for life, while waiting can increase it significantly.

In this guide, we will clearly explain the difference between claiming Social Security at age 62 vs 70, using simple numbers and real examples so you can understand what works best for you.

Why Timing Your Social Security Claim Is So Important?

You can start receiving Social Security retirement benefits as early as age 62. But if you wait until age 70, your monthly payment becomes much higher.

According to the Social Security Administration, the difference is not small—it is huge and lasts your entire life.

2026 Maximum Benefit Comparison

| Age You Claim | Monthly Benefit | Yearly Benefit |

|---|---|---|

| 62 years | $2,969 | $35,628 |

| 70 years | $5,181 | $62,172 |

| Difference | +$2,212 | +$26,544 |

That means waiting until 70 can give you over $26,500 more every year.

Average Social Security Payments (Real-Life Data)

Not everyone gets the maximum amount. Most people receive average benefits.

Here is what typical retirees get:

| Age | Average Monthly Payment |

|---|---|

| 62 | $1,424 |

| 70 | $2,275 |

| Gap | +$851 |

That is about a 60% increase just by waiting.

Also, these payments increase every year due to cost-of-living adjustments (COLA), so the gap grows even bigger over time.

How the System Works: Early vs Late Retirement?

The Social Security system is designed to reward people who wait.

Key Rules You Should Know

- Full Retirement Age (FRA): 67 (for people born in 1960 or later)

- Claim at 62 → about 30% reduction

- Delay after 67 → 8% increase per year

- Maximum increase stops at age 70

Simple Example

Let’s say your full benefit at age 67 is $2,000/month:

| Claim Age | Monthly Payment |

|---|---|

| 62 | $1,400 |

| 67 | $2,000 |

| 70 | $2,480 |

Difference between 62 and 70 = $1,080 per month

That is a big long-term gain.

Why Many People Still Claim Early?

Even though waiting gives more money, most people still claim early.

Here is what data shows:

- Around 45% claim before age 65

- About 29% claim at 62

- Only 10% wait until 70

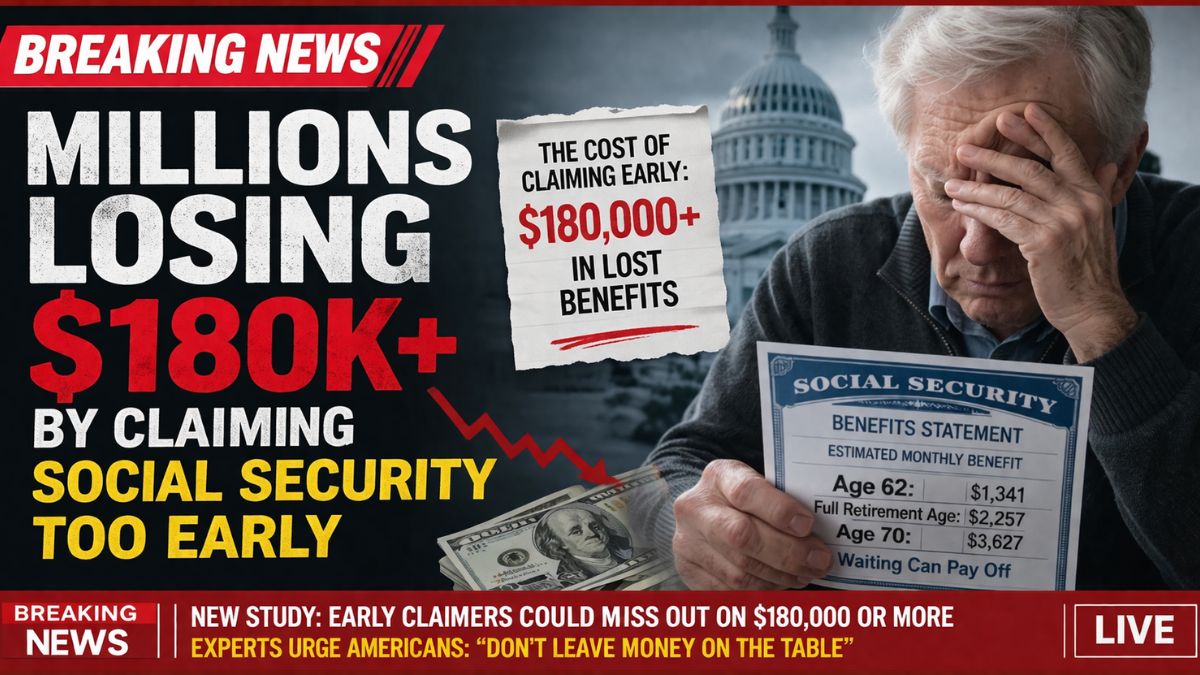

Research by the National Bureau of Economic Research shows that claiming early can lead to a lifetime loss of around $182,370.

Another study by the Bipartisan Policy Center found that the gap between 62 and 70 can reach 77% more income monthly.

Reasons Why People Choose Early Retirement

There are many real-life reasons behind this decision:

- Immediate need for money

- Health problems

- Shorter life expectancy

- Fear that Social Security may change in the future

- Lack of knowledge about how the system works

In fact, surveys show that many people don’t fully understand Social Security rules.

Should You Wait or Claim Early?

There is no single answer for everyone. It depends on your situation.

When Claiming Early Might Make Sense?

- You need money urgently

- You have health issues

- You don’t expect a long retirement

When Waiting Is Better?

- You are healthy and expect a long life

- You want higher monthly income

- You have other savings to support early years

The Social Security gap between age 62 and 70 is one of the most important financial decisions in retirement planning. Waiting can increase your monthly income by thousands of dollars and add up to hundreds of thousands over your lifetime.

However, real life is not only about numbers. Health, lifestyle, savings, and personal needs also matter a lot.

If you can afford to wait, the system clearly rewards you with higher benefits. But if you need money early, claiming at 62 still provides support.

The key is to understand how the system works and make a smart, informed decision that fits your life. Always consider speaking with a financial expert before deciding.

FAQs

Is it better to take Social Security at 62 or 70?

Waiting until 70 usually gives much higher monthly payments, but it depends on your health and financial needs.

How much do you lose by claiming early?

You can lose around 30% of your monthly benefit if you claim at 62 instead of full retirement age.

Do benefits increase after age 70?

No, benefits stop increasing after age 70, so there is no advantage to waiting beyond that.